Why now might be the best time in years to buy in Southwestern Ontario

If you've been watching the market and waiting for the “right time,” here's something that might surprise you: across much of Southwestern Ontario, the same home now costs well over $200,000 less than it did at the 2022 peak — and interest rates have come down too. Cheaper homes and cheaper money don't often show up at the same time.

We're breaking this down on AM 980 and the podcast this week. Think of this post as your quick, at-a-glance companion — the numbers, in plain language.

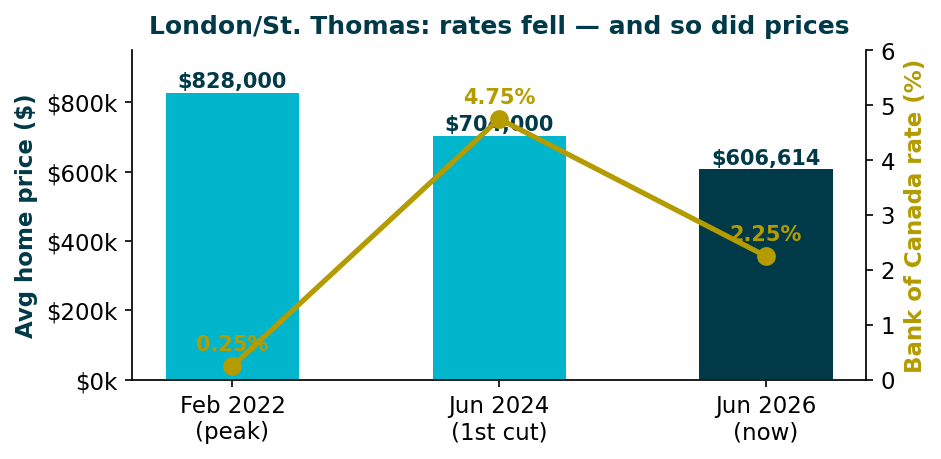

Rates came down — and so did prices

The Bank of Canada has cut its rate from 5.00% all the way to 2.25%. Here's the part most people miss: home values didn't jump when rates fell — they eased. In London and St. Thomas, the average price came off its 2022 peak of about $828,000 to roughly $606,000 today.

Rates fell — and so did prices. Buyers today get both.

That's the rare double win: a lower purchase price and a lower cost of borrowing at the same time.

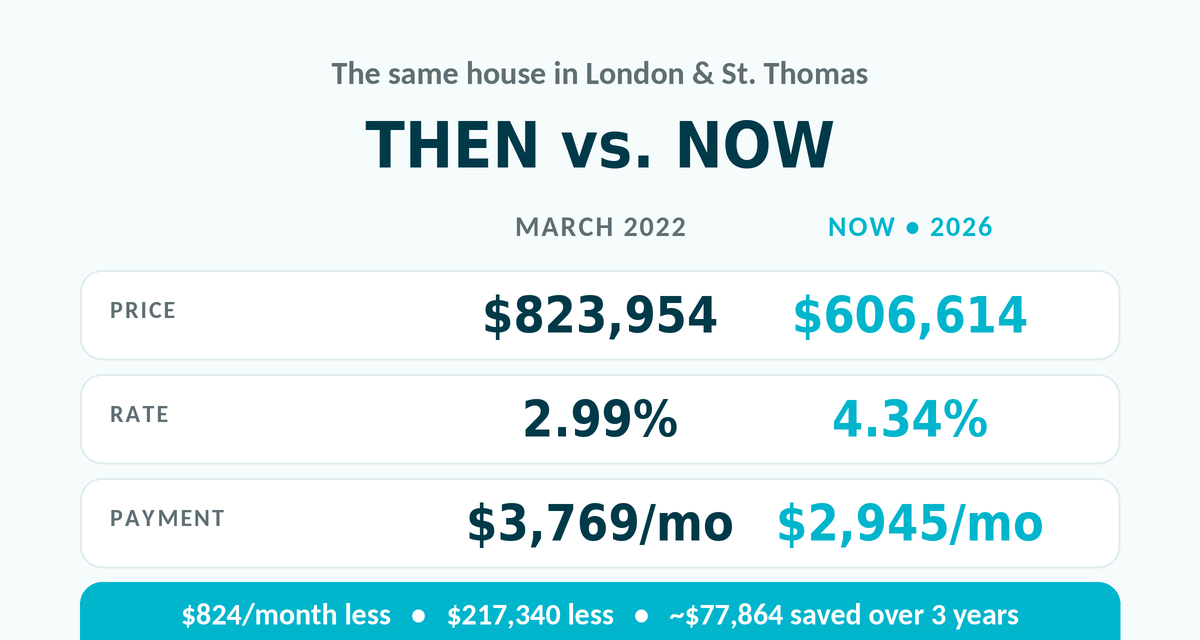

The same home, then vs. now

Numbers make it real. Take the exact same London/St. Thomas home at the 2022 peak versus today:

Even at a higher rate, today's buyer pays less each month.

Yes, the interest rate is higher today — but the price drop more than makes up for it. The monthly payment is about $824 lower, and a buyer today saves roughly $77,864 over a three-year term compared with buying at the 2022 low-rate peak.

The lesson: waiting for rates to fall can quietly cost more than buying a cheaper home now.

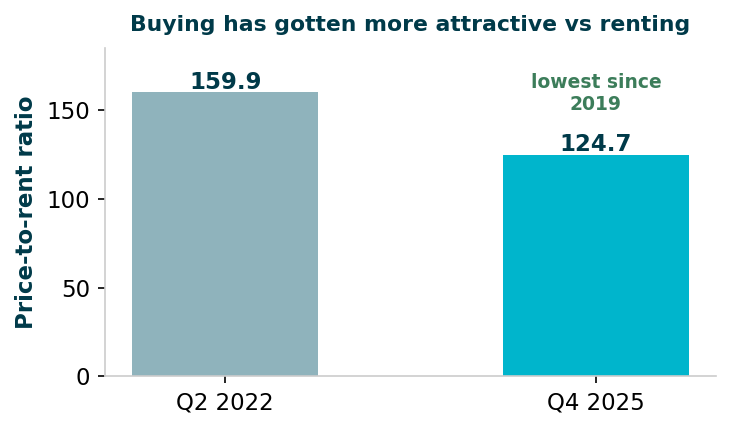

It's a buyer's market — and that's good news

For anyone who's felt priced out or rushed in recent years, the tone of the market has shifted in your favour:

Prices are off about 27% from the 2022 peak

The Bank of Canada rate is down to 2.25%

Average rents are at a 33-month low, and the price-to-rent ratio is back to 2019 levels

Fewer buyers competing means more room to negotiate

Renting vs. buying has swung back toward buying in many SW Ontario markets.

It's a calmer market, not a frantic one — which is often exactly when well-prepared buyers make their best moves.

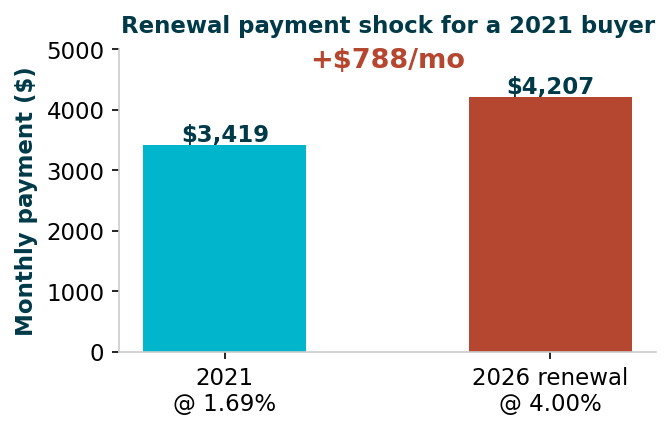

Renewing in 2026? Don't just sign.

This isn't only a buyer's story. Roughly 1.15 million Canadian mortgages come due in 2026 — 44% of them right here in Ontario. Many households are facing a real payment jump at renewal.

A typical 2021 buyer can face roughly +$788/month at renewal.

The good news: you have options. A quick conversation with a broker can soften the jump — a longer amortization, a switch to a better lender, or rolling improvements into the mortgage. The worst move is signing the first offer without shopping it.

So… why now?

Because cheaper homes plus cheaper money is a combination we don't see often. Add in rents off their highs and wages that have held up, and the window is genuinely open — for first-time buyers, move-up buyers, and anyone renewing. The opportunity is being missed by a lot of people, not because it isn't there.

Want the full breakdown? Tune in to our segment on AM 980 and the podcast this week, where we walk through exactly what this means for buyers and renewers in Southwestern Ontario.

Figures are approximate and for education only — drawn from CREA/LSTAR, the Bank of Canada, CMHC and market data. Rates and values change without notice and are not a rate guarantee or financial advice. Mortgage Teacher • Shop Smart. • FSRA #12509 • 1-855-289-2991 • mortgageteacher.com